Like every year, automobile taxation is updated and 2022 is no exception.

Here are all the changes to be aware of for fleet managers regarding the new weight penalty, TVS (or NTU), the ecological penalty and bonus, non-deductible depreciation, the benefit in kind or even VAT on fuel.

The new weight penalty in detail

The weight penalty is put in place on January 1, 2022, after being voted on in the National Assembly at the end of 2021. A measure which aims to send a signal to “stop this heavy vehicle frenzy”, declared Barbara Pompili, the Minister of Ecological Transition.

It concerns all vehicles over 1800 kg , at a rate of €10 per kilo above 1800 kg, with the exception of electric or hydrogen vehicles and plug-in hybrid vehicles whose autonomy in all-electric urban traffic is at least equal 50 km away.

Please note that the total penalty (CO2 penalty + weight penalty) cannot exceed the maximum penalty scale (€40,000 before application of VAT).

Tax on company vehicles and new use taxes

In 2022, the Company Vehicle Tax (TVS) will disappear in favor of two New Use Taxes (NTU) :

- Annual tax on CO2 emissions : operation and scale identical to the 'CO2 Tax' in force in 2021

- Annual tax on atmospheric pollutants : operation and scale identical to the 'Air Tax' in force in 2021

How to calculate TVS in 2022?

The scales communicated for the first component , the CO2 Emissions Tax, are always based on the CO2 emission rate , as previously, and correspond to a full year of use.

However, the calculation method differs depending on whether they are vehicles registered before or after March 1, 2020 (NEDC vs WLTP).

For NEDC vehicles (registered until February 29, 2020): the scale remains unchanged since 2019

For vehicles registered after March 1, 2020: a tax based on WLTP CO² is applied (lower since 2021 on the least polluting vehicles (up to 157g inclusive) = unchanged since 2021

The minimum duration of 30 consecutive days of use to be eligible for NTU is retained.

NEW :

The calculation based on the number of quarters is abandoned in favor of the number of real (calendar) days of ownership or use.

NB: the declaration of NTUs in January 2023 for the year 2022 can still be carried out, and for the last time, on the basis of quarters of use.

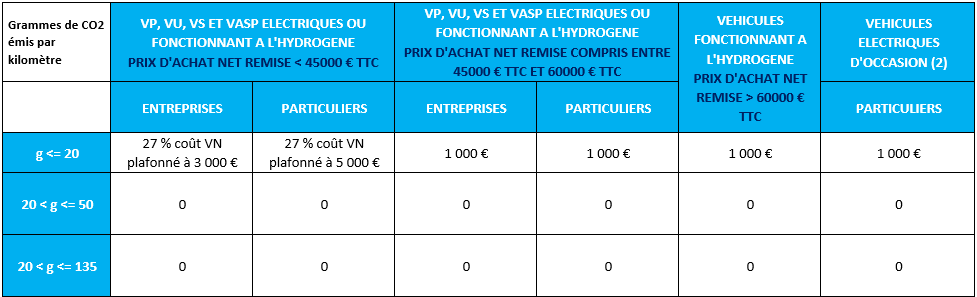

Ecological bonus 2022

The bonus in force since July 1, 2021 is extended by 6 months , making it valid until June 30, 2022 (decree 2021-1866 published on 12/29/2021).

As of July 1, 2022 :

- The bonus is reduced by €1000 for all eligible vehicles.

- The bonus intended for PHEVs (plug-in hybrid vehicles) disappears.

Here is a summary table of the 2022 bonus and its evolution throughout the year.

ECOLOGICAL BONUS FOR THE PERIOD FROM 07/26/2021 TO 06/30/2022

ECOLOGICAL BONUS FOR THE PERIOD FROM 07/01, 2022 TO 12/31/2022

(1) To be eligible for the bonus, plug-in hybrid vehicles must comply with the following three conditions: CO2 emission rate between 21 and 50 g, discounted net purchase price less than or equal to €50,000 including tax, autonomy in fully electric circulation in town strictly greater than 50 km

(2) To be eligible for the bonus, used electric vehicles must have been registered for at least 2 years.

Tightening of the ecological penalty 2022

The 'CO2' ecological penalty will tighten further in 2022 , since it:

- Starts from 128 g of CO2 (compared to 133g in 2021)

- Can amount to €40,000 (as a reminder, the maximum ceiling of the penalty was €30,000 in 2021)

However, a new rule is emerging: the penalty cannot exceed 50% of the purchase price of the vehicle . As with the calculation of the bonus eligibility price, only immediate discounts are taken into account.

| 2020 | 2021 | 2022 | 2023 | |

|---|---|---|---|---|

| CO² rate in g/km | 138 g CO² | 133 g CO² | 128g CO2 | 123 g CO² |

| Maximum penalty* | 20 000 € | 30 000 € | 40 000 € | 50 000 € |

*The CO² penalty cannot exceed 50% of the price of the vehicle including tax stored

The different exemptions for electric and hybrid vehicles

Permanent exemption:

Electric or hydrogen-powered vehicles emitting less than 20 g of CO2 are definitively exempt from the two new usage taxes .

vehicles are definitively exempt from the Annual Tax on CO2 Emissions as long as:

- Their CO2 emission rate does not exceed 50 g (NEDC) or 60 g (WLTP)

- They don't run on diesel

NB: The Annual Tax on Atmospheric Pollutants remains due for exempt hybrids.

Temporary exemption:

Temporary exemptions are maintained for 3 years for hybrid vehicles :

- As long as the CO2 emission rate is between 51 g and 100 g (NEDC) or between 61 and 120 g (WLTP)

- As long as they don't run on diesel

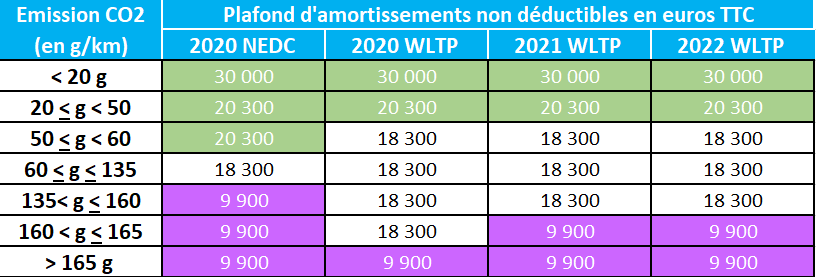

Non-deductible depreciation: the ceiling reached in 2022

The ceiling defined by the 2017 Finance Law has now been reached and is maintained for 2022:

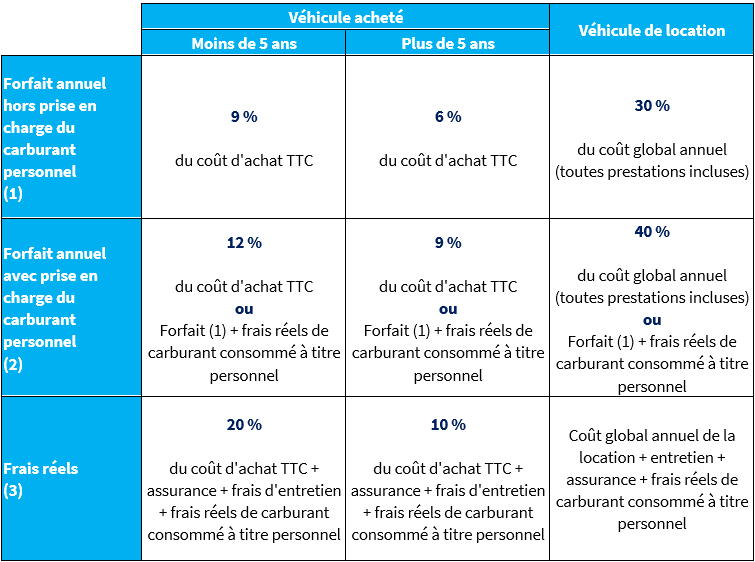

Vehicle benefit in kind

The method of calculating benefits in kind is kept the same in 2022.

Electric vehicles still benefit from:

- A 50% reduction on the amount of benefits in kind up to €1,800 per year (€150 per month) until December 31, 2022

- Top-ups paid by the employer do not increase the rate applicable to the amount of benefits in kind

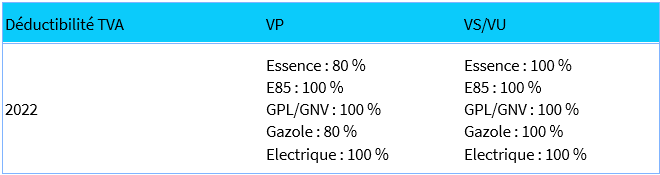

VAT on fuel in 2022

As planned for the year 2022, the VAT deductibility rate on gasoline is now 100% on Utility Vehicles (LCVs) , thus making it possible to offer the same deductibility for gasoline and diesel vehicles.

In 2022, the VAT deductibility on Petrol and Diesel Private Vehicles (PV) remains at 80%.

It amounts to 100% for vehicles running on E85 superethanol, LPG or CNG and for electric vehicles.

FATEC Group, expert in automobile fleet management, can advise and support you in the management of your fleet and its taxation.

Learn more